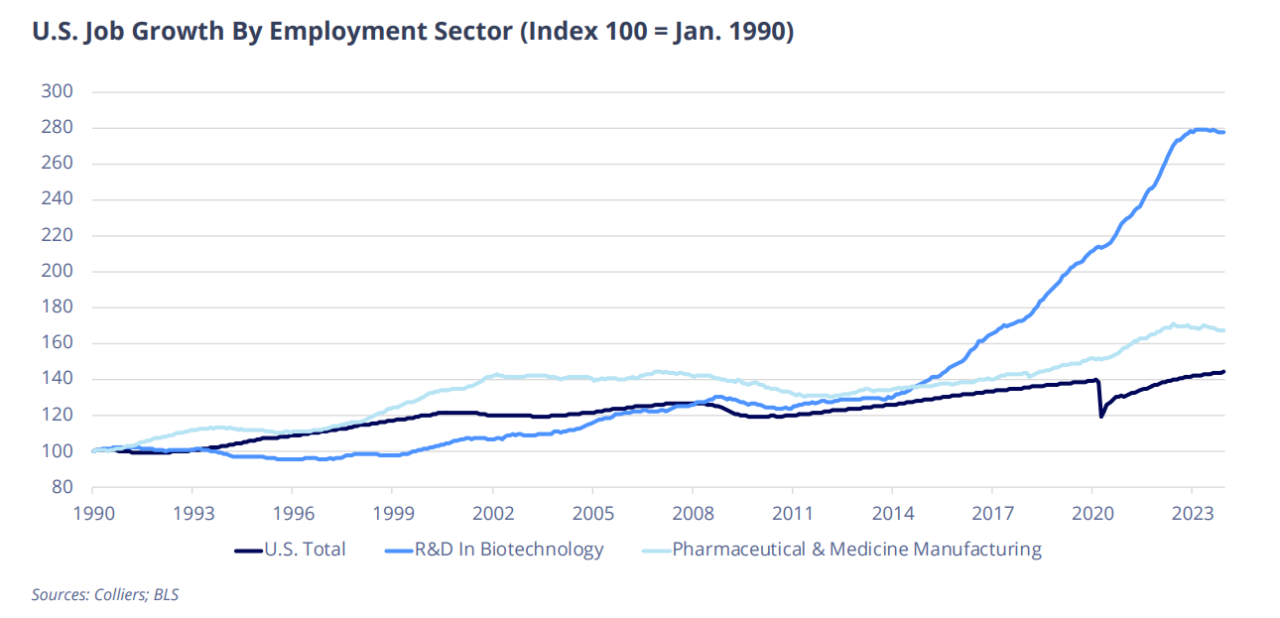

In spite of current capital markets headwinds, long-term demand drivers for the life sciences industry are strong. Per capita expenditures on pharmaceuticals have been trending upward for decades, and dozens of countries are now spending more than 1% of GDP on these products.

This is especially true in the United States, where, according to the most recent OECD data, per capita spending (excluding hospital settings) now exceeds $1,400, at more than 2% of the nation’s GDP. The industry has plenty of upside. Per the U.S. Food & Drug Administration (FDA), fewer than 10% of the approximately 7,000 known rare diseases have an FDA-approved treatment. Technological advances alongside robust demand prospects will create profitable long-term opportunities, the impetus for innovation within the industry. Real estate absorption will follow suit, as the life sciences sector is outperforming many other industries in job growth. Since 2015, more than 50 million SF of life sciences space has been absorbed across the major markets.

Funding conditions could perk up in 2024 and help give companies the confidence and ability to lease space. The Fed has paused rate hikes, however lingering inflation has dampened the potential for a significant number of rate cuts in 2024. Even so, as conditions have stabilized, the S&P Biotechnology Select Industry Index (SPSIBI) value has risen from its 2023 trough and is generally in line with its early 2020 pre-COVID level.