Summary

On Wednesday, July 31, 2024, the Federal Open Market Committee (FOMC) voted unanimously to hold the federal funds rate at a target range of 5.25–5.50%. This marks over a year and eight consecutive meetings since the Committee last adjusted the target range, having raised it to the current level on July 26, 2023. Unlike the static target range, the FOMC statement underwent several revisions.

The Committee shifted its focus from “inflation risks” to “both sides of its dual mandate.” Pundits interpreted the statement as largely neutral and in line with expectations. Meanwhile, Chair Powell’s press conference was viewed as dovish. He expressed growing confidence in ebbing inflation and reiterated the Fed’s dual mandate to maintain price stability and maximum sustainable employment.

Impact on rates

After the Committee’s statement, rates rose marginally. However, they turned negative following Powell’s press conference. Rates on the front end of the curve declined by two to 10 basis points, while the belly and the back end declined by 10 to 11 basis points.

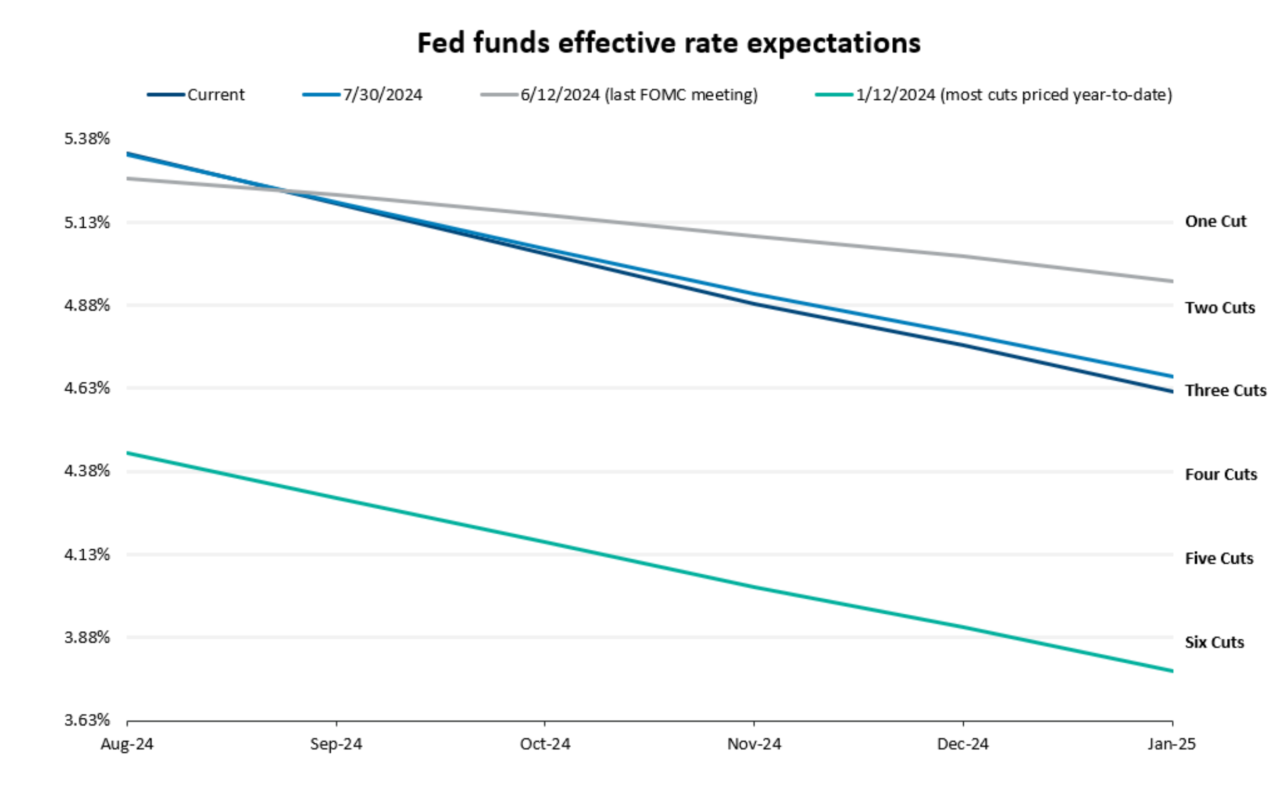

The market is now pricing roughly three cuts by the end of the year — an increase from June’s meeting but still significantly less than the start of 2024.

Moving forward

During this meeting, Powell stated that both “several or zero” cuts could occur over the remainder of the year. The Fed plans to take a step back and closely observe the data, expanding their focus beyond their recent inflation bias. The dual mandate was highlighted in both the statement and by Powell’s remarks. There is anticipation that the Fed will take a more balanced approach when considering the impact of restrictive policy on both inflation and employment. If inflation continues to trend favorably, the Fed may look toward proactive rate cuts to protect against the “long and variable lags” of monetary policy.

Source: Chatham Financial