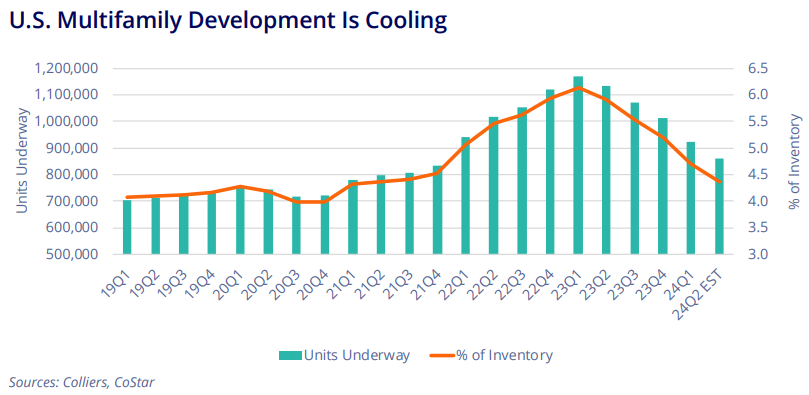

The U.S. multifamily market has faced pressure in recent quarters. Occupancies have slipped due to a rise in development, resulting in the highest levels of completion in decades. As a result, vacancies have shifted more rapidly in demographic hotspots in the Southeast and Southwest, which have seen higher supply levels than Midwest and Northeast markets. Rising operating expenses have crimped NOI, and owners are battling higher financing costs. However, occupancies are at or near their low point, with forecasts showing improvement in the quarters ahead. High home prices and owners locked into low mortgage rates will keep renters in place.

Supply-Side Pressure is Easing

Multifamily deliveries have been heavy, averaging 153,000 units per quarter over the last year through Q1. Supply has peaked, as the number of units under construction has dipped below one million for the first time since 2022 Q2. Construction starts have slowed due to higher financing costs, allowing the market to recalibrate, especially in the Southeast and Southwest, where development has been

substantial.

Management Matters

Today’s market conditions have highlighted the distinction between those with strong property management and those without it. Managers with experience in various economic cycles can effectively navigate the wave of development and the pressure on opex while still managing occupancy. This doesn’t mean occupancies haven’t fallen in the largest portfolios, but it is not uncommon for investors with short-term hold horizons to face challenges today. These groups now find themselves having to manage properties, which was not part of their initial investment strategy. In some cases, occupancies are falling more rapidly than the market overall, construction has taken longer than anticipated for renovations, and costs are higher. This situation has led to numerous current and potential failed deals, offering intriguing buying opportunities in the quarters ahead.

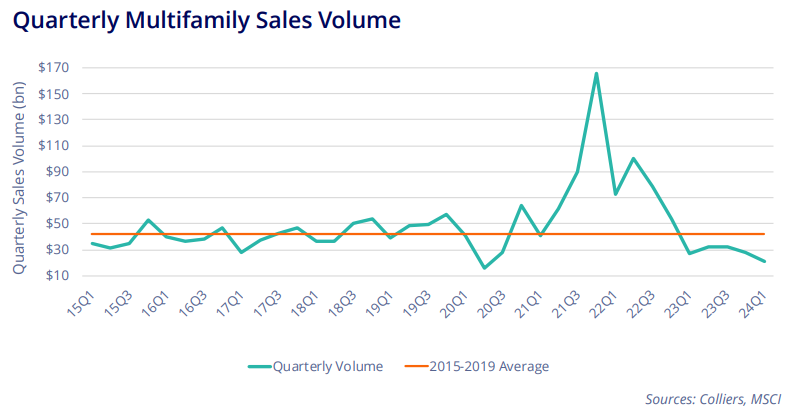

Sales Remain Limited

Investment sales volume is still trying to find an equilibrium. Multifamily remains the most heavily traded of all asset classes, so liquidity remains, though it is impaired. Given the rise in borrowing costs, investors are clamoring for assets with lower financing rates. Properties with such characteristics have been met with deep bid sheets and strong pricing. It is not uncommon for pricing to outperform expectations.