The Evolution of Artificial Intelligence: Shaping the Future of Data Centers

Once again, the data center industry had another record-setting year, and its long-term outlook remains bright. According to Statista Market Forecast, global data center market revenue is projected to have reached $325.9 billion in 2023 and, over the next five years, an annual growth rate of 6.1%, reaching $438.7 billion by 2028 — largely driven by AI.

While bandwidth and data storage consumption have spurred demand for data centers over the last decade, 2023 will be remembered as the coming-of-age year of artificial intelligence (AI). Although still in their early days, applications like ChatGPT and Dalle burst onto the scene, offering a glimpse of AI’s versatility and ability to process and analyze data, create images, improve efficiencies and decision-making, and boost overall productivity across industries. ChatGPT reached 100 million users worldwide in just two months, a goal that took Facebook 4.5 years!

The ability to scale resources on demand, critical to the rapid growth of AI, is driving demand for hyperscale cloud providers like Amazon Web Services, Google Cloud, and Microsoft Azure. As a result, hyperscalers increased their total megawatt output across North America to just over 15.2 gigawatts, 17.8% more than last year. Besides providing the computational power and scalability essential for AI and machine learning workloads, hyperscalers also excel in data storage and management, offering solutions like data lakes, databases, and data warehouses capable of handling vast amounts of data.

Supply & Demand

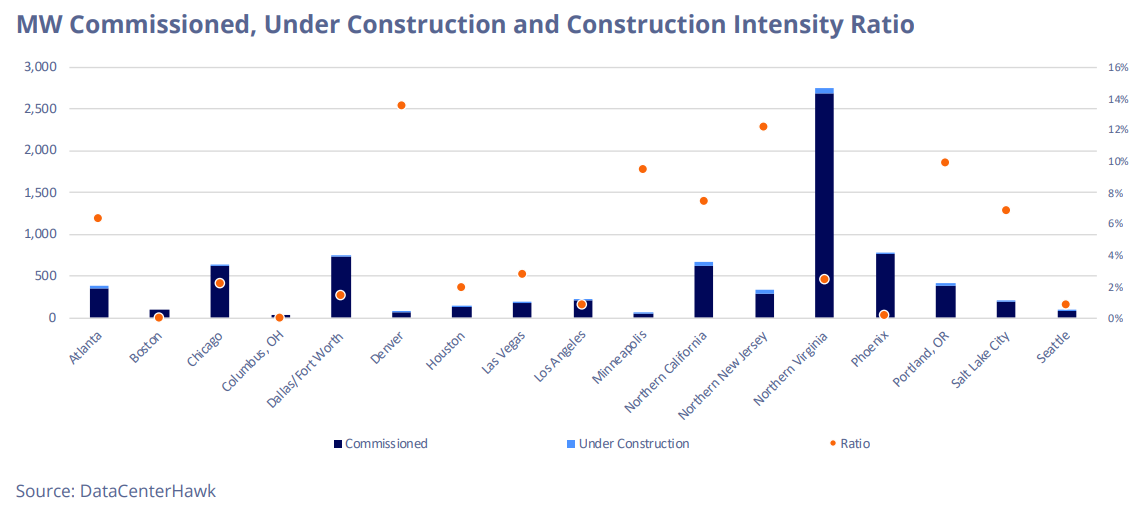

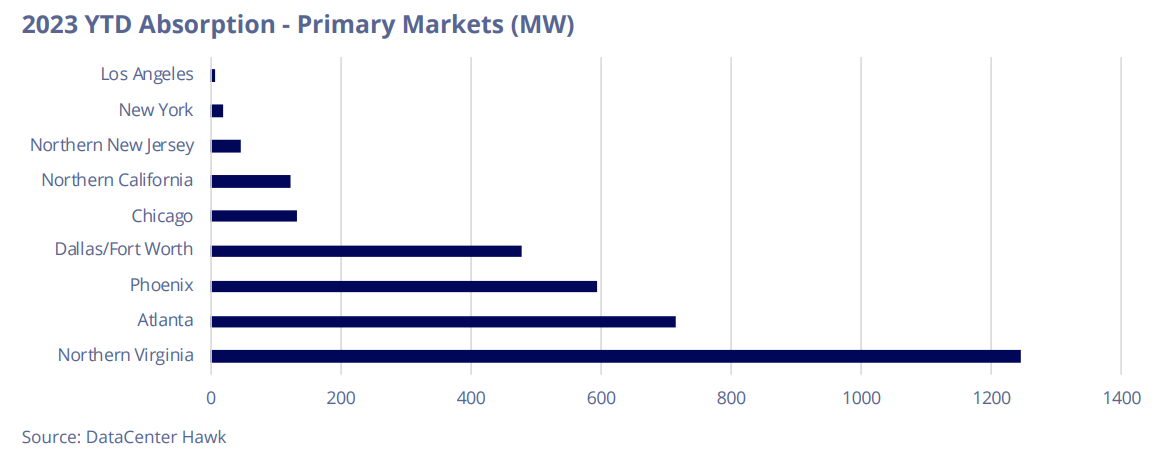

After a record-setting year in 2022, the demand for data centers shifted into high gear in 2023. Across the 19 markets tracked for this report, the overall vacancy rate dropped 200 basis points, to 1.7%, from year-end 2022. Markets less active in recent years recorded the largest vacancy declines year-over-year, including Dallas/Fort Worth (410 basis points), Houston (400 basis points), and Atlanta (380 basis points). For the fifth consecutive year, the industry set a new record for absorption, at 3,870.1 MW in 2023. Northern Virginia led all markets with 1,244.5 MW absorbed, followed by Atlanta (714.2 MW), Phoenix (594.5 MW), and Dallas-Ft. Worth (477.2 MW), most of it in new construction.

Despite record-setting demand, the total amount of power under construction declined year-over year by 68.8 MW because of a lack of shovel-ready sites, to 282.1 MW. While Northern Virginia and Northern California have long been considered essential for data product, markets

like Northern New Jersey, Atlanta, and Reno are attracting strong development, and in many instances, new starts have been preleased.