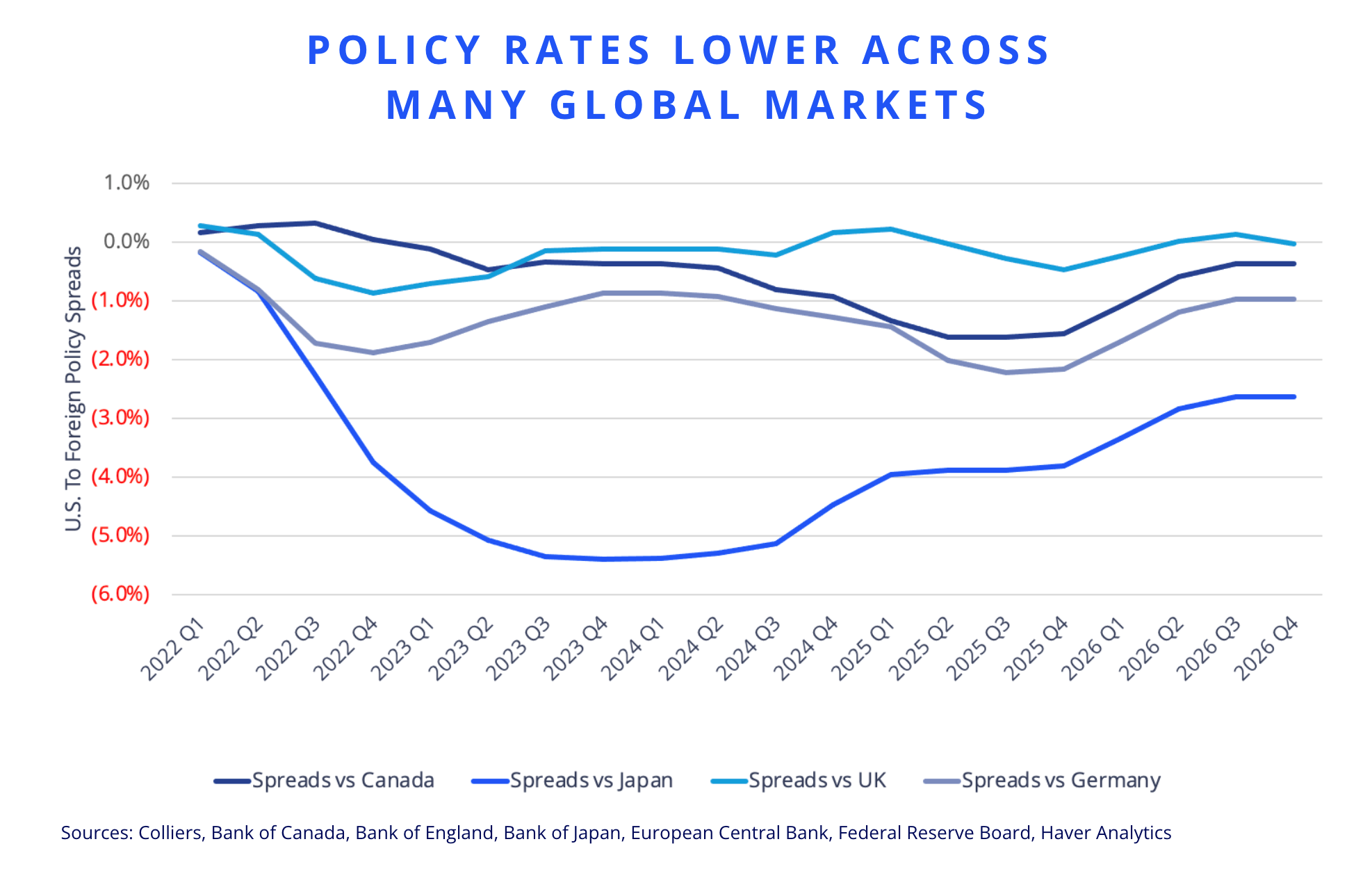

• The Federal Reserve has been more restrained in its policy movements relative to other nations and global regions.

• While rates in the U.S., Canada, and the UK were similar at the start of 2022, they have diverged of late.

• Rate cuts are improving the spreads available compared to average prime yields/cap rates in all three regions.

• Cross-border volumes into the U.S. have been limited in recent quarters.

• Attractive cap rates, especially when compared to places like Japan and Germany, could draw capital to the U.S.

Global economies have moved past the post-COVID inflation and interest rate spike,

however, managing subsequent rate cuts remains key for national and regional economies, as well as government policy. As of May, EMEA and the Eurozone appear best positioned to sustain lower interest rates. The European Central Bank (ECB) and Bank of England (BoE) each began 2025 with a 25-basis-point cut, with the BoE cutting another 25 basis points in May. The inflation outlook for Europe looks subdued, and the BoE is projected to cut rates two more times during 2025, with only one additional cut expected from the ECB.

North America’s policy outlook is mixed. In the U.S., inflation has remained stubborn, with current policies potentially leading to both inflationary and deflationary outcomes. For example, a minimum 10% tariff application points to imported inflation. The consensus is that the Fed may deliver only one additional rate cut in 2025. Canada lowered its benchmark rate by 25 basis points in January, with further reductions likely this year.

In APAC, Japan is slowly raising rates as core inflation remains elevated. South Korea, Australia, and Singapore began cutting rates in Q1, with more moves likely as the economic outlook weakens.

Rate cuts are improving the available spreads relative to average prime yields/cap rates in all three global regions. APAC yield spreads remain most favorable, while EMEA and North America have seen marked improvements since late 2024, notably in terms of spreads to central bank policy rates. Overall, spreads to policy rates, assuming a 50% LTV position, are more than sufficient to support strong transactional activity in all three regions.

The U.S. is the number one source of global capital at 28%, nearly three times that of second-place, Canada.

However, spreads to 10-year government bonds remain thin in both EMEA and North America. This raises doubts about the relevance of traditional risk-adjusted pricing mechanisms, a concern heightened by sovereign credit downgrades. As a result, it is hindering institutionally driven real estate investment in particular. Cross-border volume into the U.S., as a share of overall volume, has been hovering near all-time lows.

While the U.S. remains the top source of capital investing in other markets, the UK is now the top destination for cross-border capital overall. Germany and Japan rank third and fourth. Low domestic rates in many countries could draw renewed interest in U.S. real estate from yield-seeking investors.

Source: Colliers