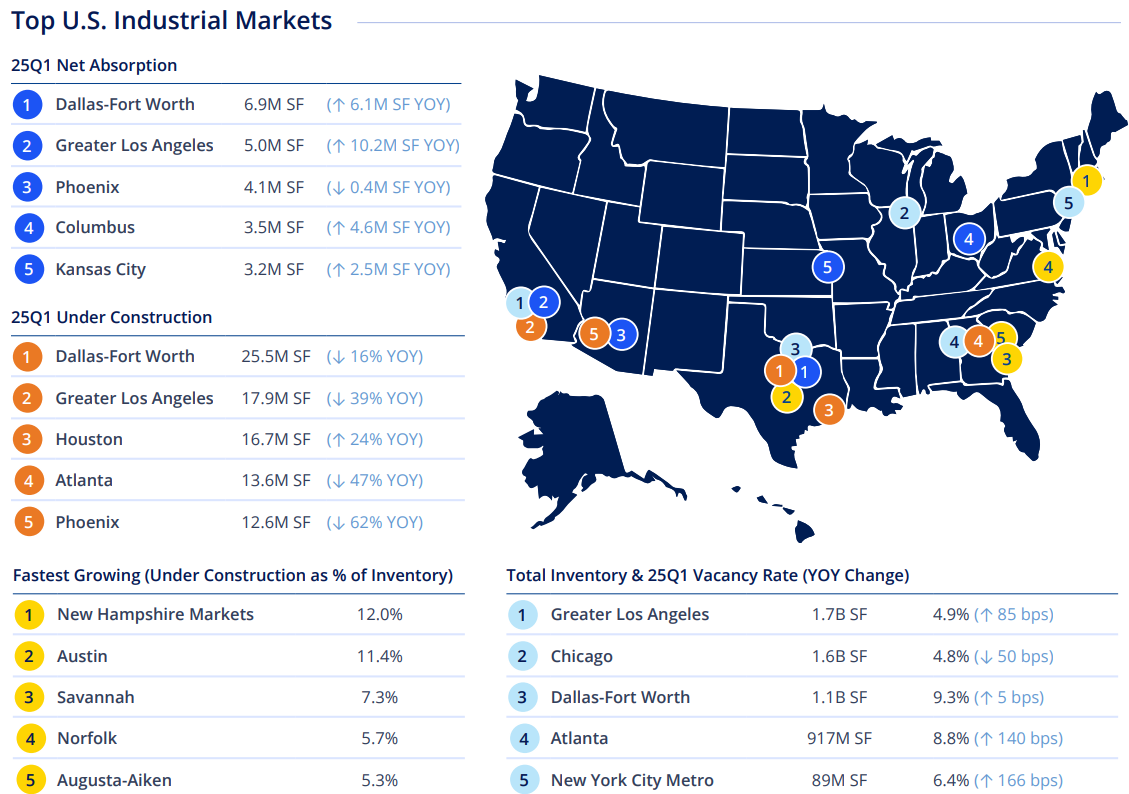

Key Takeaways

• New supply pushed vacancy up slightly by 14 basis points to 7.1% during the first quarter, the highest level since 2015.

• Supply and demand fell more in line, largely due to construction completions dropping to 65M SF.

• Construction slowed to 279M SF, 61% below its peak of 711M SF and still falling.

• Rents grew in some markets and decreased in others but are expected to stabilize in 2025.

Industrial vacancy to peak in 2025 as equilibrium returns

New supply has outpaced demand during the past 11 quarters, pushing the average U.S. industrial rate up 351 basis points during that time, to 7.1% —the highest level since 2015. However, vacancy increased by just 14 basis points in the first quarter, the smallest quarterly increase since the fourth quarter of 2022. Across all U.S. regions, vacancy rates are rising more gradually, because construction completions are falling below pre-pandemic levels, narrowing the gap between supply and demand. Stabilization is expected by the end of 2025, with vacancy expected to peak due to a significantly reduced construction pipeline.

New supply of 65M SF, the lowest quarterly total since the first quarter of 2019, was 60% below the peak of 163M SF in the third quarter of 2023. Demand as measured by net absorption fell to 35M SF, 34% below last quarter, but still 12% higher than in the first quarter last year. Both indicators are expected to align more closely during 2025 when the current development cycle winds down. Although the uncertainty about the economy, tariffs, and policy duration may delay a significant rebound in demand over the coming quarters, net absorption is expected to remain positive through the end of 2025.

Source: Colliers